TalkMed Group Ltd - An Amazing Net Profit Generator

After writing about BBR Holding (S) Ltd, I got a request from a friend to review on TalkMed Group Ltd.

He said it was my "kinda" of company.

Thus, I look at its latest financial report and it got me interested.

Profile In Short

TalkMed Group Limited is mainly involved in providing cancer related medical services and operates a network of 8 clinics in Singapore.

Recently it has collaboration with overseas companies (Hong Kong) to expand their services and also went into Stem Cell and Stem Cord services.

(At this point, I am already at "WOW"!)

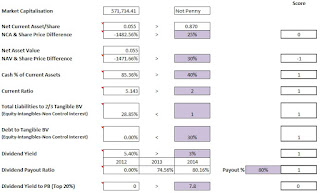

Based on Triple S Scorecard:

It failed - despite showing that it had a strong balance sheet and good earnings ability. This is most probably due to the price being too high.

I am really interested in this business and company. The business environment has been right as well. However, if you read into my analysis, other than failing the Triple S Scorecard, there are too many questions that remained unanswered. The company has only been listed for 1 year plus and does not have much historical records to really justify the current "still" very high price.

Look at the SGX, how many listed medical provider (Other than Raffles Medical) actually went on and become a good company that rewards shareholders eventually?

Current Price: 0.87 as of 21 Feb 2016

Please do your own due diligence before you invest in this stock.

Do note the author is NOT vested in this stock/company.

So if you are interested in my Triple S Scorecard, contact me through my blog or message me on my T.U.B Investing Facebook Page.

As for the online course, its on! Contact me if you are interested. Furthermore, we are thinking of changing it into a full fledge course (still in the mist of preparing).

Do like our facebook page too...

He said it was my "kinda" of company.

Thus, I look at its latest financial report and it got me interested.

Profile In Short

TalkMed Group Limited is mainly involved in providing cancer related medical services and operates a network of 8 clinics in Singapore.

Recently it has collaboration with overseas companies (Hong Kong) to expand their services and also went into Stem Cell and Stem Cord services.

(At this point, I am already at "WOW"!)

Based on Triple S Scorecard:

It failed - despite showing that it had a strong balance sheet and good earnings ability. This is most probably due to the price being too high.

Why So Good?

Medical Services - The company mainly provides medical services and research mainly related to cancer. This business is very lucrative and you should understand why.

High Net Profit Margin and Strong Balance Sheet - The company shows its earning ability (net profit is consistently higher than 50%) and balance sheet strength (very low liabilities) as per Triple S Scorecard.

Expansion into Stem Cell and Stem Cord - If you understand cancer as an illness, it is mainly due to bad cells in the body (I think). By creating new cells to replace the bad cells, a patient may get better (I am not a doctor and these are just my assumptions....correct me if I am wrong.)

Why So Bad?

Rise since IPO Price - The company has rise over 400% in 1 day since IPO price of 20 cents. On what basis did those people have at that time? At 0.870, the price is still significantly higher than the IPO price of 0.20. Another question arises - Why did the placement price during IPO at 20 cents only? Is there something we don't know?

Lock Up Period Over - The end of the lock up period for 110,400,000 shares of TalkMed Group Limited is at 30 Jan 2016. This is about 16% of the outstanding number of shares the company has. After the lock up period, the shares started coming down. Is there any insider selling?

Cost Deeply Related To Remuneration Of Doctors - One of the major cost of the company is the Remuneration of the Doctors. If one day, one of the main doctors request for an extensive pay rise, the company will not be able to reject them.

Company Deeply Related With Reputation Of Doctors - What happens if the reputation of the main doctor is in question? As per reported in SGX Announcement, there was an inquiry on Dr. Ang Peng Tiam in May 2015.

Expansion "Too Fast Too Furious" - In 2015, the company has expanded overseas, collaterated with other cancer centres and went into stem cell and stem cord. Will the company be able to handle these businesses and if the company have enough man-power to handle them as well? In addition, how will these additional cost impact their Income Statement? Will the cost escalated faster than the Revenue?

In Short

Look at the SGX, how many listed medical provider (Other than Raffles Medical) actually went on and become a good company that rewards shareholders eventually?

Current Price: 0.87 as of 21 Feb 2016

Please do your own due diligence before you invest in this stock.

Do note the author is NOT vested in this stock/company.

So if you are interested in my Triple S Scorecard, contact me through my blog or message me on my T.U.B Investing Facebook Page.

As for the online course, its on! Contact me if you are interested. Furthermore, we are thinking of changing it into a full fledge course (still in the mist of preparing).

Do like our facebook page too...

Comments

Post a Comment