TUB Snippets 4: Forgotten Healthcare Companies in SGX

For those who are new to the blog, I have three on-going series: 10X Potential Series, Portfolio Update, and TUB Snippets.

In short, it operates 3 segments - medical centers/clinics, healthcare system and Med investments - and is located in 4 countries (Philippines, Indonesia, Singapore and Hong Kong).

TUB Snippets are for companies that I've looked into (but not necessarily invested in) and want to share my brief thoughts on.

Please note that I no longer own any of the businesses mentioned in the past TUB Snippets.

Today, I will be writing about these 3 forgotten healthcare companies in Singapore.

1. Offer Announced - Singapore O&G Ltd (SOG)(Ticker: 1D8)

Basically the Group gets S$0.295-a-share takeover offer from vehicle linked to Dymon Asia.

Based on the FY2021 results of EPS of 1.75 cents and NAV of 10.25 cents (Singapore dollars), this will be PE of 16.85x and PB of 2.87x.

Thus, my opinion is that this PE and PB can be taken as a market standard moving forward for medical group with specialized services.

2. Omicron Wave - Healthway Medical Corporation Ltd (HWM)(Ticker: 5NG)

When looking at the entire healthcare industry on the SGX, HWM stands out since it is more focused on general practitioner clinics.

I have a preference for general practitioner clinics in Singapore due to the crazy queues in these clinics nowadays with the Omicron Wave, as well as the Singapore subsidies for patients visiting these clinics.

|

| Image taken from Straits Times Article in May 2021 |

|

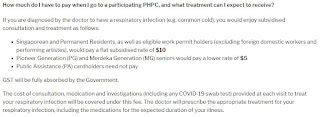

| Image taken from Singapore Government PHPC FAQ on the Singapore Subsidies |

Based on the FY2021 results, HWM has a PE of 14.17x and PB of 0.82x. These ratios are relatively lower than the PE and PB of SOG.

Furthermore, the closest competitor in SGX is probably Raffles Medical Ltd (RM) with PE of 25.6x and PB of 2.2x.

Some may argue PB may not be a good indicator due to the high intangibles in HWM balance sheet. Regardless, HWM's PE is still lower than SOG's and RM's PE.

It is important to note that:

- HWM own, operate and manage 98 clinics and medical centres in Singapore - being the largest outpatient clinic chain in Singapore.

- HWM has 51 of its clinics being PHPC and also operate 2 quick test centres.

- Acquired another primary healthcare chain of 9 clinics in Sep 21 (included in point 1).

- HWM began administering the first batch of Sinopharm COVID19 vaccines in Sep 21. The cost is S$99 per 2 doses.

- Based on FY2020 Annual Report, 40.91% is controlled in the hands of James and Stephan Riady.

- Their business is highly defensive against inflation and recession scenarios.

Given the foregoing and the current scenario in Singapore, it appears that HWM is likely to be undervalued if its top and bottom lines continue to grow with at least an expected PE of 16x.

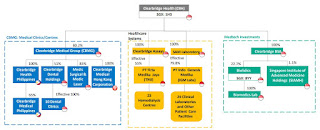

3. Turnaround Story - Clearbridge Health Limited (CBH)(Ticker: 1H3)

CBH recently released its FY2021 results - it looked terrible on an accounting basis with S$34m revenue and S$18m of losses. But if added back the depreciation and impairment, the adjusted Ebitda is actually S$1m.

|

| CBH Latest Corporate Presentation 1 |

|

| CBH Latest Corporate Presentation 2 |

In short, it operates 3 segments - medical centers/clinics, healthcare system and Med investments - and is located in 4 countries (Philippines, Indonesia, Singapore and Hong Kong).

There are 2 important information that investors need to take note:

Indonesia healthcare system business

- As per FY2020 presentation, it is a (1) 5 to 10 years (2) recurring income business model, with (3) estimated 70% revenue sharing with IGM Labs and TMJ and (4) services being reimbursed by Indonesia health coverage program.

- With Jokowi being elected in 2019 as the President of Indonesia for another 5 years (till 2024), the national health insurance implemented by him should still be in effect till at least end 2023.

Sole importer and distributor of Labnovation’s COVID-19 ART Test Kits in the Philippines

- Only two COVID-19 ART Test Kits, one by Labnovation and the other by Abbott Panbio, that have been recently approved by the FDA of the Philippines for self-testing.

- Philippines has a population of 110 million with over 3.4 million of confirmed Covid-19 cases.

- From these 2 articles (1 and 2), it is understood that there are still another 31 brands of ART kit waiting to be approved, but there is a price cap to of P660 (S$17.15) on the ART Kit, with manufacturer cost capped at P350 (S$9.10) and mark up by distributor at P60 (S$1.56).

- In this case, CBH has a competitive advantage in this segment with a first mover advantage.

The next financial reporting end Jun 2022 will be in Aug 2022. If CBH continues to provide positive updates prior to Jun 2022, CBH downtrend share price could be at an inflection point.

With that, I hope to bring these companies to your attention.

If you had read till here and I have value-added to your investment journey, please support by clicking into the Google Ads if it interest you!

Appreciate!

Stay tuned for the next write up!

Comments

Post a Comment